Explore the comprehensive history of banking in India. From the indigenous moneylenders and the British Presidency Banks to the 1969 Nationalization and today's UPI revolution. A deep dive into the evolution of the Indian financial system.

Introduction: The Roots of Trust

The story of banking in India is not merely a chronicle of financial institutions, interest rates, and regulatory acts. It is, at its core, the story of India itself—a narrative of empire and independence, of socialism and liberalization, of ancient trust and modern technology. From the indigenous money lenders of the Vedic era to the algorithmic trading of Mumbai’s Dalal Street, the evolution of Indian banking mirrors the shifting tides of the nation’s socio-political identity.

To understand where we stand today, with Unified Payments Interfaces (UPI) and neobanks, we must first look back to a time when credit was a matter of word and honor, long before the first marble facade of a European bank rose on the shores of Bengal.

Chapter 1: The Indigenous Era (Ancient Times to 18th Century)

The Moneylenders and the Guilds

Long before the British East India Company set foot on the subcontinent, India possessed a sophisticated system of credit and currency. The Vedas (2000–1400 BCE) are the earliest texts to mention usury (kusidin), indicating that lending money for interest was a recognized, albeit sometimes frowned upon, profession. By the Mauryan period (321–185 BCE), the Arthashastra by Chanakya laid down regulatory frameworks for interest rates and loan deeds, treating banking as an integral part of the state machinery.

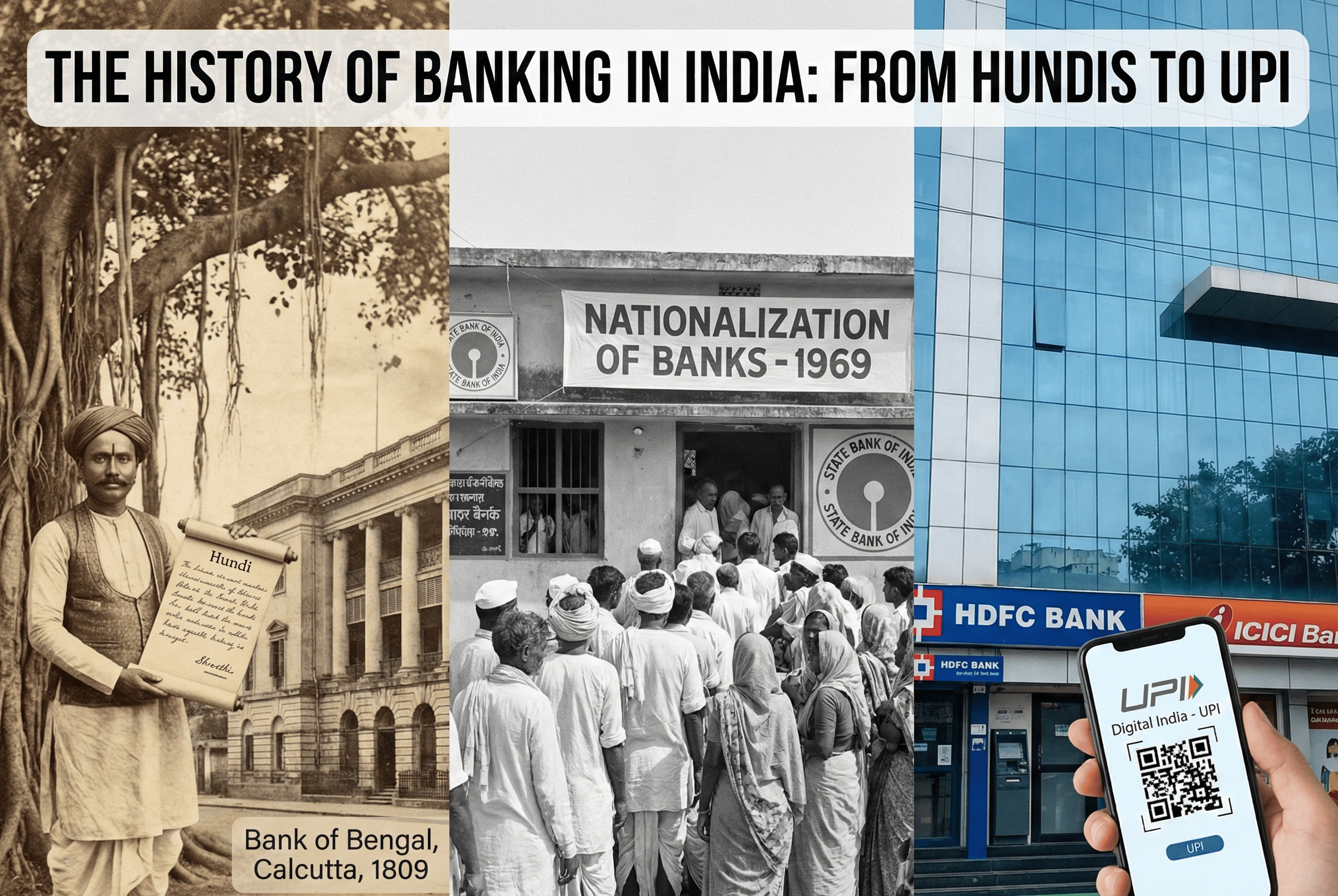

In this era, banking was not institutionalized in buildings but embodied in communities. The Shresthis (Seths) of North India and the Chettiars of the South were the bankers of the day. They issued Hundis—financial instruments that functioned as bills of exchange. A merchant in Pataliputra could deposit gold with a Shresthi and receive a Hundi, which could then be encashed in Taxila. This system, relying entirely on the reputation of the issuer, greased the wheels of trade along the Silk Road and the spice routes.

During the Mughal era, these indigenous bankers became incredibly powerful. The house of Jagat Seth (Banker of the World) in Bengal is the most illustrious example. They were effectively the state treasurers, handling tax revenue and remitting funds to Delhi. Their financial clout was so immense that they could make or break Nawabs. It is often said that the Battle of Plassey in 1757, which established British rule in India, was financed not just by the East India Company, but by the betrayal of the Jagat Seths, who sided with Clive against Siraj-ud-Daulah.

However, this indigenous system was fragmented. It lacked a unified currency and a central authority. As the sun set on the Mughal Empire and rose on the British, the nature of banking was about to change largely.

Chapter 2: The European Experiment (1770–1860)

Agency Houses and the Failure of Early Ventures

The arrival of the British brought the concept of "joint-stock banking." The indigenous bankers, while efficient, operated on personal capital and unlimited liability. The British needed banks that could aggregate capital from many investors to fund their expanding trade and colonial wars.

The first such attempt was the Bank of Hindostan, established in Calcutta in 1770 by the agency house of Alexander & Co. It was a European-style bank, serving the needs of the European community. However, it could not withstand the panic of 1829–32 and collapsed. Another early venture, the General Bank of India (1786), also failed.

This period was characterized by volatility. These banks were essentially tied to the trading fortunes of the East India Company’s servants. When trade boomed, banks flourished; when wars or mismanagement struck, they crumbled. There was no "Lender of Last Resort"—no central bank to save them.

Chapter 3: The Presidency Banks (1806–1920)

The Foundations of Modern Banking

Realizing the need for stable institutions to manage government finance and currency, the East India Company moved to establish quasi-central banks. These were the Presidency Banks, named after the three administrative units of British India.

Bank of Calcutta (1806): Later renamed the Bank of Bengal in 1809. It was the first government-chartered bank.

Bank of Bombay (1840): Established to serve the trade interests of western India.

Bank of Madras (1843): Serving the southern peninsula.

These three banks were unique. They had the right to issue currency notes (until 1861), they held the government’s balances, and they managed the public debt. They were the giants of the 19th century, funded by both government and private shareholders.

However, the "Paper Currency Act of 1861" was a turning point. The British government took away the right of note issuance from these banks, vesting it solely in the state. This stripped the Presidency Banks of a major power but forced them to focus on deposit banking and lending, maturing their business models.

The late 19th century also saw the birth of banks owned and managed by Indians, fueled by the rising Swadeshi sentiment. The Allahabad Bank was established in 1865 (the oldest joint-stock bank in India still functioning until its recent merger). The Punjab National Bank (PNB) was founded in 1894 by Lala Lajpat Rai and others, solely with Indian capital and management. These were not just financial institutions; they were symbols of national pride.

Chapter 4: The Imperial Bank and the RBI (1921–1947)

Centralization and the Birth of a Guardian

As the 20th century dawned, the flaws of the Presidency Bank system became apparent. There was little coordination between Bengal, Bombay, and Madras. To create a unified banking giant, the three Presidency Banks were amalgamated in 1921 to form the Imperial Bank of India.

The Imperial Bank was a strange beast—it acted as a commercial bank for the public and a central bank for the government. But this dual role was problematic. How could a bank compete with other commercial banks while also regulating them?

The need for a distinct, independent central bank became undeniable. Following the recommendations of the Hilton Young Commission (1926), the Reserve Bank of India (RBI) was established on April 1, 1935.

The birth of the RBI was a watershed moment. Finally, India had a supreme authority to regulate the issue of banknotes, maintain reserves, and operate the currency and credit system. Initially, the RBI was a shareholder's bank, but its mandate was public service. It took over the central banking functions from the Imperial Bank, leaving the latter to focus purely on commercial banking.

The pre-independence era closed with a banking sector that was urban-centric, class-biased, and prone to failure. Between 1913 and 1948, approximately 1,100 small banks failed in India. The system was fragile, serving the elite and ignoring the masses.

Chapter 5: Independence and the Social Control Era (1947–1969)

Building a Nation, One Branch at a Time

When India awoke to life and freedom in 1947, its banking system was deeply disjointed. The partition of India dealt a severe blow, particularly to banks in Punjab and Bengal, where assets and customers were suddenly divided by a bloody border.

The new Indian government, led by Jawaharlal Nehru, viewed banking as a tool for economic development. The first major step was the Nationalization of the RBI in 1949. The Banking Regulation Act of 1949 followed, giving the RBI sweeping powers to license, inspect, and regulate banks.

In 1955, the government took another giant leap. The Imperial Bank of India, the largest commercial bank, was nationalized and renamed the State Bank of India (SBI). Its mandate was specific: to expand into the rural heartland where private banks feared to tread.

Despite these efforts, by the 1960s, banking was still an exclusive club. Industry received 68% of total bank credit, while agriculture—the backbone of the economy—received less than 2%. Private banks were controlled by large industrial houses that funneled public deposits into their own companies. The "social control" of banks became a political rallying cry.

Chapter 6: The Great Nationalization (1969–1980)

Indira Gandhi’s Gamble

On the night of July 19, 1969, Prime Minister Indira Gandhi made a radio address that changed the financial landscape forever. She announced the nationalization of 14 major commercial banks. These banks held 85% of the country’s bank deposits.

The stated goal was to break the nexus between banks and big business and to direct credit toward "priority sectors"—agriculture, small-scale industries, and exports. Overnight, bankers became public servants. The profit motive was replaced by social welfare targets.

The impact was immediate and massive. Branch expansion exploded. Banks opened in remote villages where the only concrete structure was the temple. The "Lead Bank Scheme" was introduced, assigning specific districts to banks to ensure development.

In 1980, six more banks were nationalized. By now, over 90% of the banking sector was under government control. This era democratized banking. The rickshaw puller and the farmer could now walk into a bank. However, it also introduced inefficiency, bureaucracy, and political interference in lending, sowing the seeds of the Non-Performing Asset (NPA) crisis that would haunt the sector decades later.

Chapter 7: The Era of Reform (1991–2000)

Liberalization and the New Private Sector

By 1991, India was facing a balance of payments crisis. The economy was stifled, and the banking sector was lethargic. Customer service was abysmal, technology was non-existent (ledgers were still handwritten), and unions were powerful.

The Narasimham Committee (1991) was set up to overhaul the system. Its recommendations were radical:

Reduce the government’s stake in public sector banks.

Stop using banks as a bottomless purse for the government (by lowering the SLR and CRR).

Open the door to private and foreign players.

This marked the beginning of Phase III: The New Generation Private Banks. In 1993-94, the RBI issued licenses to new players. Enter HDFC Bank, ICICI Bank, Axis Bank (UTI), and IndusInd Bank.

These banks brought a revolution. They introduced Core Banking Solutions (CBS), ATMs, internet banking, and a service culture that stunned the Indian consumer. Suddenly, you didn't have to plead with a surly teller to withdraw your own money. The competition forced public sector banks (PSBs) to wake up and modernize.

Chapter 8: The Digital Revolution and Inclusion (2000–2016)

From Brick and Mortar to Bits and Bytes

The early 2000s were defined by the rapid adoption of technology. The Real Time Gross Settlement (RTGS) and National Electronic Funds Transfer (NEFT) systems made moving money across the country instantaneous.

However, a large part of India remained "unbanked." In 2014, the government launched the Pradhan Mantri Jan Dhan Yojana (PMJDY). It was the world's largest financial inclusion program. Zero-balance accounts were opened for hundreds of millions of poor Indians.

While many accounts remained dormant initially, they laid the "rails" for the Direct Benefit Transfer (DBT) system, ensuring government subsidies went directly to the poor, bypassing the leaky bucket of corruption.

Chapter 9: The Modern Era (2016–Present)

De-monetization, UPI, and Consolidation

The night of November 8, 2016, saw another shock: Demonetization. While its economic success is debated, it undeniably forced a cash-heavy nation toward digital payments.

This coincided with the rise of the Unified Payments Interface (UPI). Developed by the National Payments Corporation of India (NPCI), UPI is perhaps the most significant contribution of India to the world of fintech. It allowed a vegetable vendor to accept payments via a QR code, democratizing digital commerce.

Simultaneously, the government began a massive consolidation of Public Sector Banks. In 2017, the SBI associates were merged into the parent SBI. In 2019 and 2020, mega-mergers reduced the number of PSBs from 27 to just 12. The goal was to create "global-sized" banks capable of funding massive infrastructure projects.

The NPA Crisis:

The last decade also saw the RBI, under Raghuram Rajan and later Urjit Patel, declaring a war on bad loans. The Asset Quality Review (AQR) forced banks to stop hiding bad debts. This led to massive reported losses but cleaned up the balance sheets. The Insolvency and Bankruptcy Code (IBC) of 2016 gave banks a legal tool to recover dues from defaulting corporate giants.

Conclusion: The Road Ahead

Today, Indian banking stands at a fascinating crossroads. It is a hybrid system where the State Bank of India—a direct descendant of the colonial Bank of Calcutta—competes with nimble fintech startups.

We are entering the era of Neo-Banks (banks without physical branches) and CBDCs (Central Bank Digital Currencies like the e-Rupee). The "JAM Trinity" (Jan Dhan, Aadhaar, Mobile) has connected over a billion people to the financial grid.

From the indigenous Shresthis issuing handwritten Hundis to a street vendor accepting a payment on a smartwatch, the journey of Indian banking is a testament to the nation’s resilience. It has moved from exclusion to inclusion, from class banking to mass banking, and from the ledger book to the blockchain. The history of Indian banking is not just about money; it is about the changing value of the Indian dream.